|

On November 22, 2013 at 2:23PM Seeking Alpha's Market Currents reported the following IBM falls as Druckenmiller makes short case - Hedge fund manager Stanley Druckenmiller has called IBM (IBM-1.5%) one of the "more high probability shorts" he's seen in years, and declares Amazon Web Services (AWS) is "killing" the IT giant.

- He's also critical of Big Blue's slumping free cash flow, and its efforts to boost flagging growth via M&A.

- AWS is expected to pull in less than $4B in revenue this year, but isgrowing at a rapid clip. In addition, analysts have argued every IT dollar eaten up by cloud services results in a greater amount of on-premise IT spend being lost.

- IBM recently bought Web hosting/cloud infrastructure provider SoftLayer for a reported $2B in order to better take on Amazon, as well as rivals such as Microsoft, Google, VMware, and Rackspace.

- Though off its October lows, IBM remains down 5% YTD in a year during which the Nasdaq is up over 30%. Shares were hit hard last month by a Q3 revenue miss.

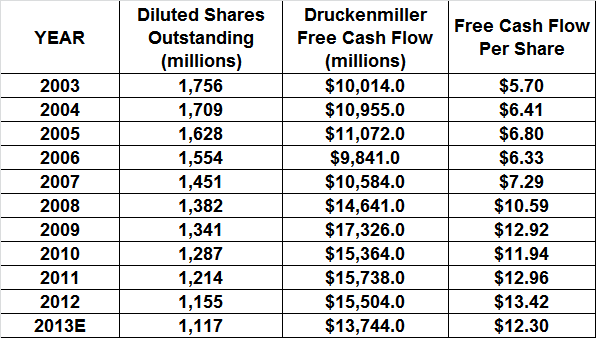

I have great respect for both Mr. Druckenmiller and Mr. Buffett and thought it would interesting to analyze each of their viewpoints in a side by side comparison and try to determine who is right on IBM. In this article I will only concentrate on the second bullet point in the Seeking Alpha Market Current above. The main point of disagreement here concerns free cash flow and despite what most investors believe, free cash flow can be calculated in a variety of ways. If we take the most common way of calculating free cash flow, which we will call for purposes of this exercise "Druckenmiller Free Cash Flow", we get the following results for IBM, (click to enlarge) As you can see, for the year 2013, Mr. Druckenmiller is correct in his statement (second bullet point) as IBM's free cash flow is definitely "slumping" and that its free cash per share number for 2013 should be lower. As an investor you have to ask yourself, what is Mr. Buffett thinking in making IBM one of Berkshire Hathaway's (BRK.A) (BRK.B) largest holdings? But before I show you, I need to give you a little background on how Mr. Buffett and Mr. Charlie Munger calculate free cash flow or what they call "Owner Earnings." On February 27, 1987 Warren Buffett released his 1986 Letter to Shareholders as part of the Berkshire Hathaway Annual Report for that year. That letter was probably one of his better-known pieces written as CEO of Berkshire Hathaway because it included a special section at the very end called: Purchase-Price Accounting Adjustments and the "Cash Flow" Fallacy Mr. Buffett provided, in essence, a tutorial on how both he and Charlie Munger select the important information in a company's financial statements. In doing so, he basically gave us their formula on how to successfully analyze companies. Here is that paragraph: If we think through these questions, we can gain some insights about what may be called "owner earnings." These represent (A) reported earnings plus (B) depreciation, depletion, amortization, and certain other non-cash charges such as Company N's items (1) and (4) less (C) the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume. (If the business requires additional working capital to maintain its competitive position and unit volume, the increment also should be included in . However, businesses following the LIFO inventory method usually do not require additional working capital if unit volume does not change.)Our owner-earnings equation does not yield the deceptively precise figures provided by GAAP, since must be a guess - and one sometimes very difficult to make. Despite this problem, we consider the owner earnings figure, not the GAAP figure, to be the relevant item for valuation purposes - both for investors in buying stocks and for managers in buying entire businesses. We agree with Keynes's observation: "I would rather be vaguely right than precisely wrong."

From Mr. Buffett's statement above we now have an additional way of calculating free cash flow or "owner earnings" as Mr. Buffett calls it. This formula when broken down to its core ingredients is very different from the calculations that are commonly used by analysts on Wall Street in calculating free cash flow. The Druckenmiller Free Cash Flow that we used above is calculated in this way; Cash Flow From Operations - Capital Spending Owner Earnings on the other hand is calculated as follows: Net income + (depreciation + depletion & amortization) + other non-cash charges - maintenance capital expenditure - increase or decrease in working capital The difficult part in Mr. Buffett's Owner Earnings calculation is that he has to factor in changes in working capital, which are not a one-step process, but require the following items to be factored in: Increases/Decreases in the following: - Receivables

- Inventories

- Pre-Paid Expenses

- Other Current Assets

- Payables

- Other Current Liabilities

- Other Working Capital

And then factor in other Non-Cash Items like stock based compensation for example. Using Mr. Buffett's owner earnings formula, the results for IBM are shown in the following table: (click to enlarge) Therefore you can clearly see that Mr. Buffett bought in heavy on IBM as his owner earnings calculations show that IBM is actually growing very quickly. In conclusion there is a wide gap between the two methodologies of calculating free cash flow as demonstrated above. Wall Street in performing its own due diligence must decide whom they will back, but history has shown us that Mr. Buffett is right most of the time. On the other hand Mr. Druckenmiller is a billionaire in his own right and did not get there by being wrong. In my own research I have come up with an additional way of analyzing free cash flow and have a "Mycroft Free Cash Flow Per Share" estimate of $16.75 for IBM for the year 2014. I have detailed how I go about calculating that result in a recent IBM article that I published on Seeking Alpha that you can read by going here . I also recently took advantage of the sharp drop in IBM's share price, after the last earnings report, and happily bought IBM for my clients at a price that was very close to what Mr. Buffett paid a few years back and feel that I bought those shares at a great bargain price. If Mr. Druckenmiller is simply using the standard way of calculating free cash flow that is very common on Wall Street, then he could be setting himself up for a lot of disappointment as very few investors have successfully come out ahead going short on a holding that Mr. Buffett owns. In my opinion there are easier ways to make money. |

狗仔卡

狗仔卡 发表于 2013-11-22 08:56 AM

发表于 2013-11-22 08:56 AM

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡

发表于 2013-11-23 10:09 PM

发表于 2013-11-23 10:09 PM