|

|

> >

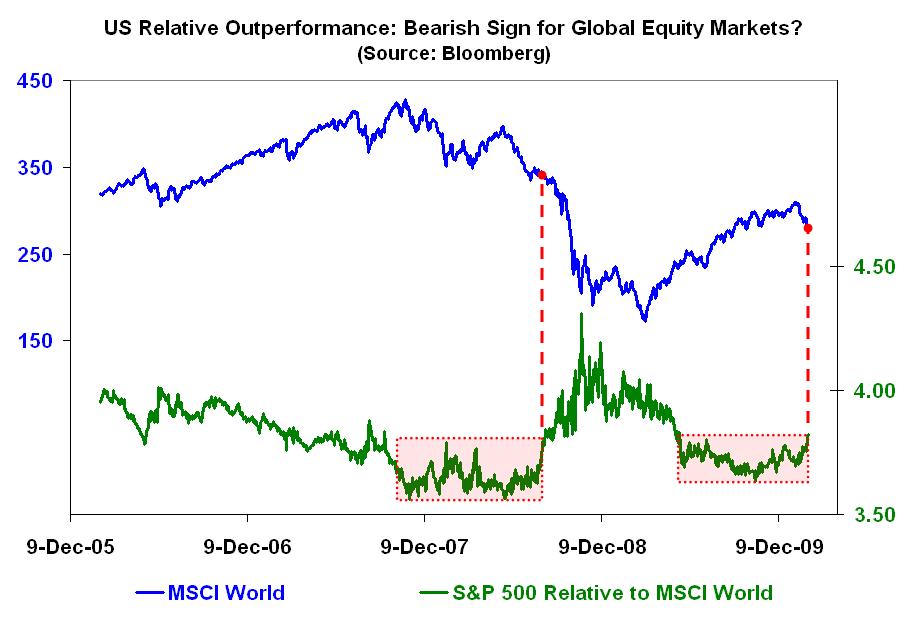

The last time the ratio of the S&P 500 to the MSCI World indexstaged a bullish breakout was in the summer of 2008 — just beforeglobal equity markets fell off a cliff.

On it’s face, that doesn’t seem to make sense. For one thing, itcontradicts anecdotal and other evidence that the U.S. tends to leadthe way as far as equity markets are concerned.

In addition, the fact that America has been ground zero in terms ofthe financial crisis would seem to indicate that our markets shouldbear the brunt when investors run scared.

That has not been the case, however. As paradoxical as it sounds,there are two reasons why U.S. markets can outperform at a time ofwidespread de-risking — or, if you prefer, panic selling.

First, the U.S. has traditionally been seen as a global safehaven.So, while investors here and elsewhere might be cashing in some oftheir chips, those international fund managers who must remain investedin equities tend to shift funds towards more defensive locales — likethe U.S.

What’s more, over the past ten months and in the period precedingthe bursting of the credit bubble in 2007, data on mutual fund andother investment flows revealed that U.S. investors sent a lot of moneyoverseas in a quest for higher returns.

But when return of capital suddenly becomes more a lot moreimportant than return on capital, the direction of those cross-borderflows can quickly change course.

In sum, things are not always what they seem.

By Michael Panzner |

|

狗仔卡

狗仔卡 发表于 2010-2-11 06:43 PM

发表于 2010-2-11 06:43 PM

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡